Executive Summary: No. Attach the briefest possible truthful reason why the return was filed late. Don’t ask that penalties not be assessed and don’t try to establish reasonable cause.

The rest of the story:

This is one of the most frequent questions I hear during my consultations with tax return preparers and exempt organization officers who are faced with having to file a Form 990 after the due date: They want to know if they should attach to the return a reasonable cause statement as to why the return was late and ask that penalties not be assessed.

I’m going to explain why attaching a reasonable cause statement is a waste of time and may not be a great idea.

This question arises, I think, largely because the instructions to Form 990 provide the following instructions:

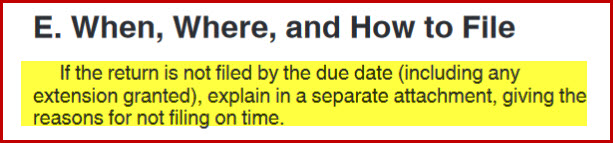

“If the return is not filed by the due date (including any extension granted), explain in a separate attachment, giving the reasons for not filing on time.”

Instructions from Form 990.

This certainly sounds like the IRS is giving the organization an opportunity to provide reasonable cause and request that penalties not be assessed.

Further, the IRS website has at some point in the last few years, revised their guidance regarding filing a return after the due date. Previously, there was no mention of attaching a reasonable cause letter to Form 990. Now the following language appears on the IRS web site: https://www.irs.gov/charities-non-profits/exempt-organizations-annual-reporting-requirements-filing-procedures-abatement-of-late-filing-penalties

From the IRS website, June 2016. The highlighted statement was added in a revision of unknown date.

The above guidance seems to reinforce and even clarify the content of the statement that is supposed to be attached to the late-filed Form 990.

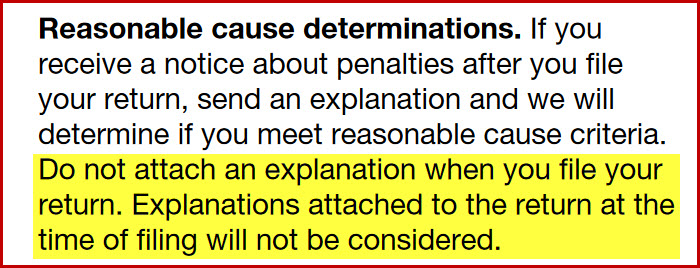

However, even clearer, and entirely contradictory guidance more in line with my personal experiences and with the conversations I’ve had with IRS personnel is found, not in the Form 990 instructions or on the IRS web site, but in the instructions to Form 8868, Extension of Time to File an Exempt Organization Return:

“Do not attach an explanation when you file your return. Explanations attached to the return at the time of filing will not be considered.”

Instructions from Form 8868.

The instructions to Form 990 and on the IRS web site seem to be in conflict with the instructions to Form 8868:

“…explain in a separate attachment…” and “…statement should be made as an attachment to the Form 990” vs. “…do not attach an explanation…”

The purpose of attaching an explanation for the late filing seems to be that of public disclosure. Information on the 990 is largely intended to provide accountability to donors. The donors have a right to know why the return was not filed on time. On many occasions over the years I have seen organizations attach to a late-filed return a reasonable cause statement and a request that penalties not be assessed. Never have these attachments resulted in the non-assessment of penalties.

I have spoken to IRS representatives in Exempt Organizations Account Services who have told me that any reasonable cause statements with requests for abatement or non-assessment of penalties that might be attached to the return are not read or processed by the IRS. That’s just not the way it works.

While it may be honorable to disclose to donors the reason a return was filed late, the detail required to make a successful reasonable cause argument may result in the disclosure of information that is unnecessary to be made public. Remember that anything attached to an exempt organization return (except donor names on Schedule B) is made available to the public. My recommendation is that the briefest possible explanation be attached to the return to comply with the IRS requirement that an explanation be attached. Once the organization has been assessed a penalty, it is then time to write a proper and thorough request for abatement of late-filing penalties under the reasonable cause provisions of IRC section 6652. (Note that section 6652 has recently been revised.)

It is helpful to understand that a request for abatement under the reasonable cause provisions must contain the following elements to be considered:

- It must be in writing.

- It must explain the reason that the return was late and explain why “reasonable cause” exists and provide credible information or documentation.

- It must be signed under penalty of perjury, with a statement such as the following: “Under penalty of perjury, I declare that the facts presented here are, to the best of my knowledge and belief, true, correct and complete.”

From the Treasury Regulations under section 301.6652-1(f):

“An affirmative showing of reasonable cause must be made in the form of a written statement, containing a declaration that it is made under the penalties of perjury, setting forth all the facts alleged as a reasonable cause.”

Of course there are many more things that go into a successful letter, which is more art than science. If you need help with a reasonable cause letter, I provide a very helpful “blueprint” in the form of a book and sample letters, all of which were actually used and were successful in having penalties abated. And I’m always available to review your letter, or write it for you if you don’t have the time, or don’t consider yourself a writer.

Comments are closed.